PepsiCo today

As of 10/10/2025 at 04:00 PM ET

- 52 week range

- $127.60

▼

$177.50

- Dividend yield

- 3.79%

- P/E ratio

- 28.53

- Price target

- $158.25

PepsiCo Nasdaq:Bib The deep discount will soon evaporate because the stock price is disconnected from reality, and the third quarter earnings report backs this up.

Trading at about 17 times current year earnings expectations and 11 times 2035 expectations, the stock is at the lower end of its historical range and poised for a cyclical rebound that could double its price over the next few years.

Historical averages put PepsiCo stock closer to a 25x valuation, with the upper limit above 30x, where it will likely reach before the next cycle is complete.

Here’s a look at why.

PepsiCo’s diversified model sustains growth, and acceleration is expected

PepsiCo’s FQ3 results prove its strength Flexibility of its diverse model. The company posted systemwide growth of 2.7%, beating the MarketBeat consensus by a narrow margin, with strength in the core beverage and international markets leading it. Sectorally, PepsiCo Foods North America was the weakest, with an organic contraction of 3%, while most other companies posted low to moderate organic growth. PepsiCo Beverages North America grew 2%, driven by gains of 5.5% and 4% in the Europe, Middle East, Africa and Latin America segments. Portfolio reshaping has also been cited as a business driver.

Margin news is also useful for shareholders and stock price forecasts. The company experienced margin pressure as expected, but not as severe as feared, resulting in operating income declining by only 1.5% and adjusted earnings by 2%. The important detail is that earnings and cash flows have been sufficient to maintain the company’s financial health while returning capital to shareholders, and the guidance outlook is optimistic.

PepsiCo’s Q4/FY guidance isn’t amazing, expecting only a single-digit organic revenue increase and a slightly narrower margin, but it has two things going for it. The first is that 2025 results are consistent with capital return expectations, which expect $8.6 billion in returns this year, and the second is that management is focused on accelerating growth, including increasing pipeline innovation, improving operational quality, and continuous portfolio optimization.

PepsiCo’s return on capital for 2026 is reliable

PepsiCo Dividend Payments

- Dividend yield

- 3.79%

- Annual profits

- $5.69

- Increasing track record profits

- 54 years old

- Dividend distribution ratio

- 103.64%

- Recent dividend payment

- September 30

PEP Dividend Date

PepsiCo’s return on capital includes dividends and stock repurchases. the Annual profits of up to more than 4% in early October 2025 and is expected to grow annually.

PepsiCo is the dividend king, with more than 50 years of consecutive annual dividend increases. The risk for investors lies in an increase in the pace of dividends or a slowdown in share buybacks.

As it stands, the company is running a single-digit dividend CAGR and is reducing the number of shares by about 0.5% each year.

The balance sheet is in good shape, although debt will increase in 2025. Regardless, assets and equity are growing as well, with equity up about 8% year-to-date, and leverage remains low. Long-term debt is less than 2.5 times equity and 1 times assets, leaving the consumer staples business in a resilient financial position.

Institutions bought PepsiCo in 2025, sparking its recovery

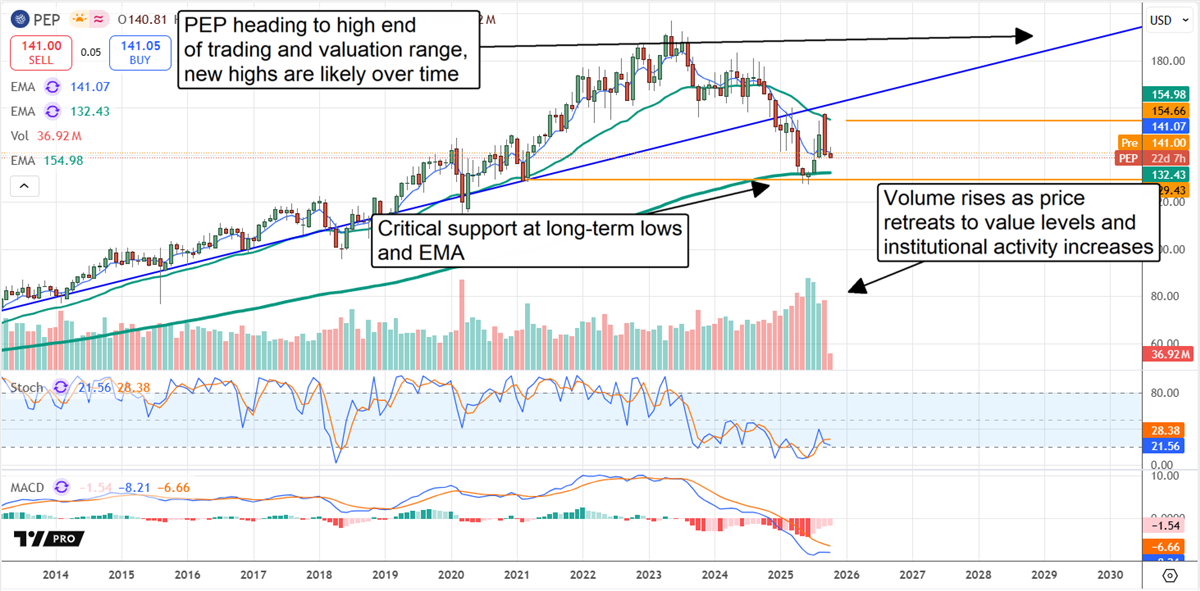

Institutional activity corresponds to PepsiCo’s price movement in 2205, indicating a market bottom. Institutions bought aggressively every quarter of 2025, including the first week of Q4, making more than $2 worth of shares for every dollar sold. They provide strong support due to this activity and ownership percentage exceeding 70% of the shares. Investors may expect this trend to continue through the end of the year, and perhaps not slow down until the PEP moves above the $155 level and the midpoint of the long-term trading range.

the The stock price movement is upward After the release, indicating support at the bottom of the long-term trading range. Assuming the market follows the signal, it should start bouncing soon and will likely enter an uptrend before the end of the year. The stock price will rise to the critical resistance level near $155 in this scenario and may continue to rise if the global economic outlook does not deteriorate.

Before you consider PepsiCo, you’ll need to hear this.

MarketBeat tracks the highest-rated and best-performing research analysts on Wall Street and the stocks they recommend to their clients on a daily basis. MarketBeat identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches up… and PepsiCo wasn’t on the list.

While PepsiCo currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View the five stocks here

Are you thinking about investing in Meta, Roblox, or Unity? Enter your email to learn what street investors need to know about the Metaverse and the public markets before making an investment.